The Trouble with Transformers

And the long slouch towards cyberpunk

For a rich country, it’s surprising how the US keeps finding itself wanting for fundamental equipment. It is one thing for a shortage to last for a few days or weeks. When it drags on for years, it points to a fundamental problem. In this case, a problem with energy and specifically the physical infrastructure of the grid. Thanks to electric vehicles and AI data centers, we are asking the grid not just to grow, but to grow faster. The grid’s physical components are well understood with many competitive suppliers. Yet lead times and prices keep increasing, resulting in cost overruns and extreme delays to grid expansion. This situation, with transformers specifically, is a testament to American sclerosis. But the news is not all bad: fixing it is within our power, and innovation is coming to help. A country that can build the world’s most advanced AI models but can’t get an electricity transformer delivered in under two years is not a country with a technology problem. It’s a country where the machinery of abundance has been taken apart, piece by piece, by people who did not build it, some who actively resent it, and were never asked to put it back together.

Surging Demand for Power, Even Before AI

For the first time in my adult life, demand for energy supplied through the electric grid is going up in the US. Electrification is driving the growth (i.e. shifting demand from fossil fuels to the grid) and now AI data centers. Grid planners assume stable, predictable growth of both supply and demand. It has been anything but.

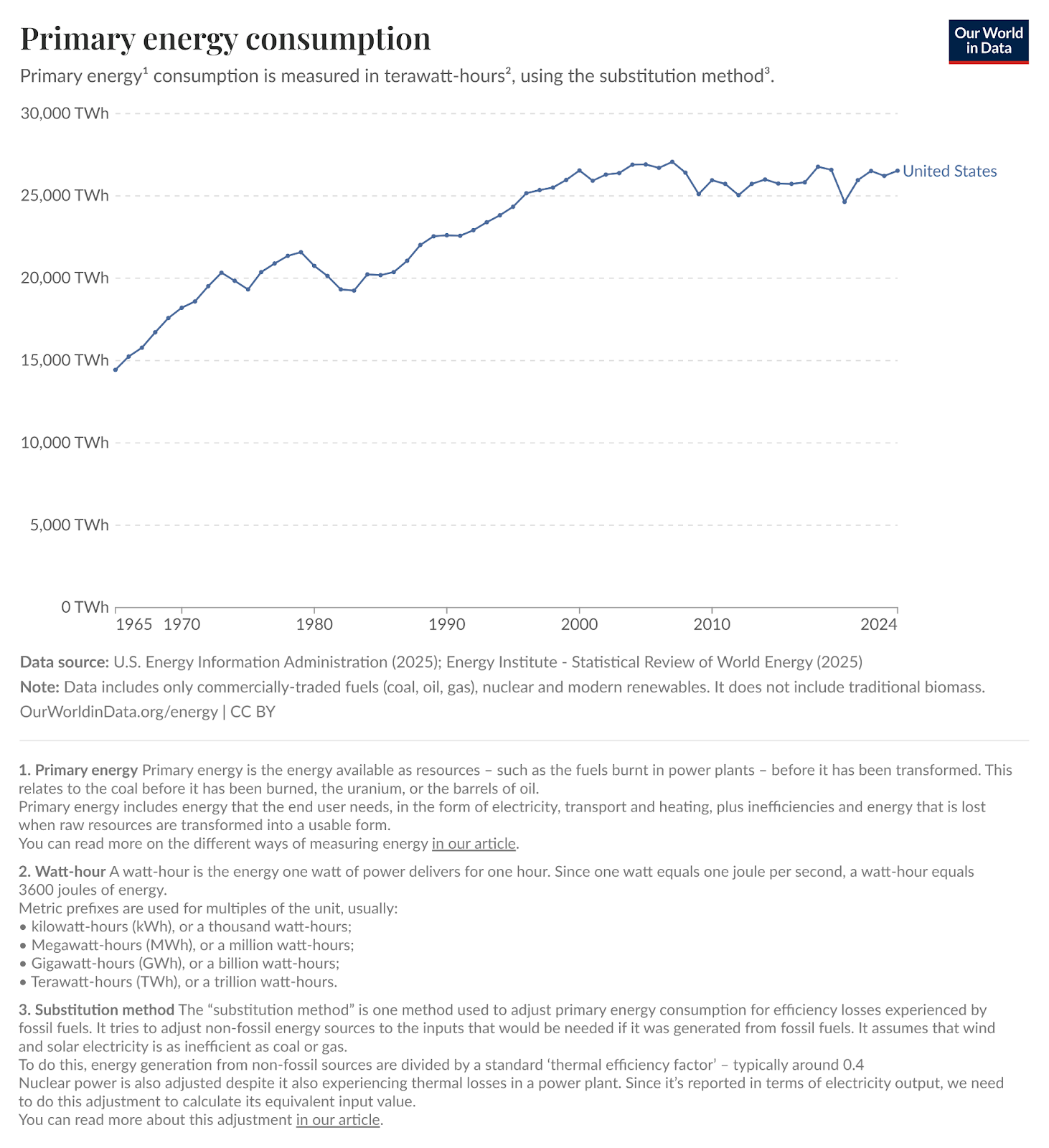

Notably, the total amount of energy consumed, including electricity, transport, and heating, is mostly stable.

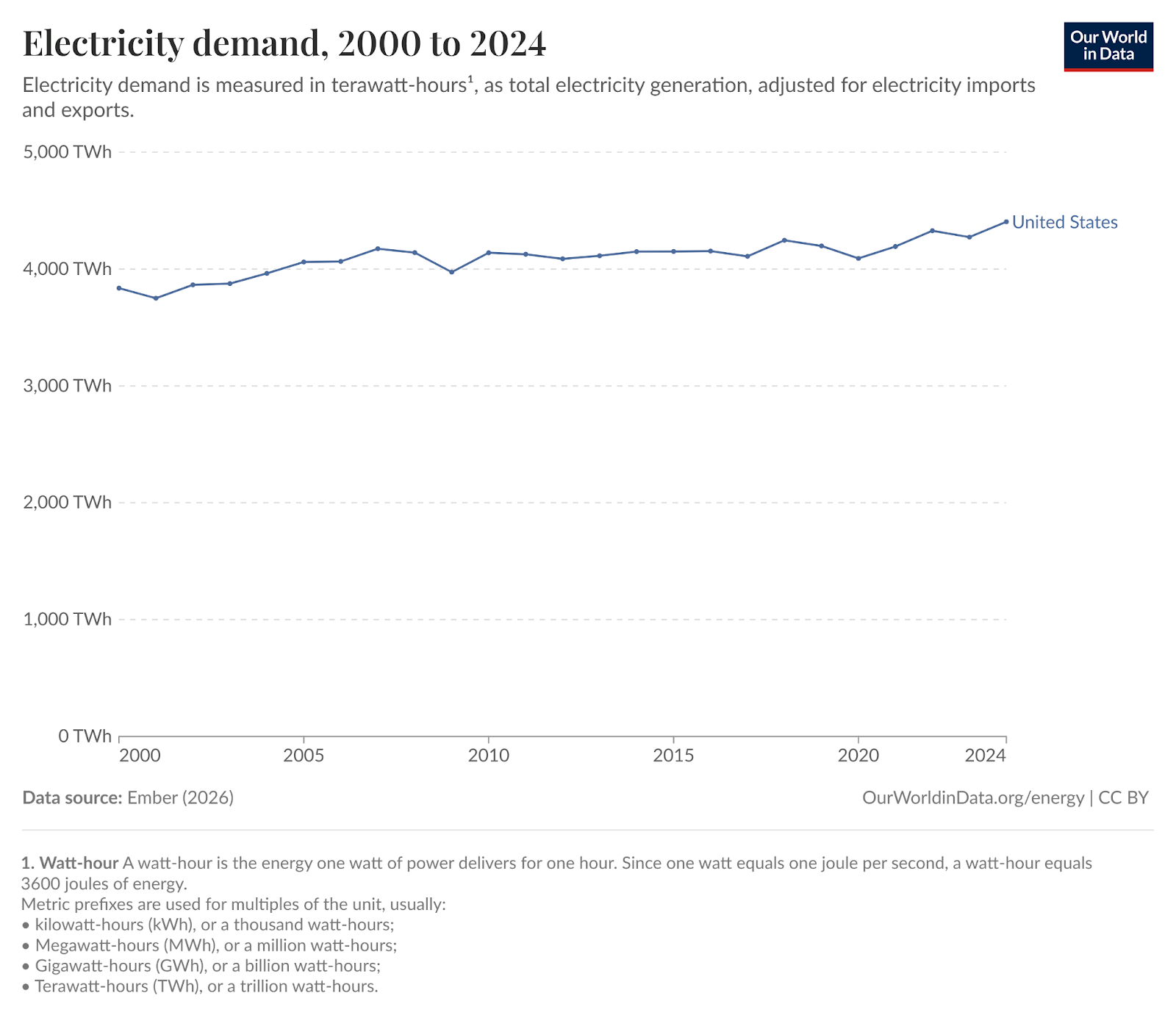

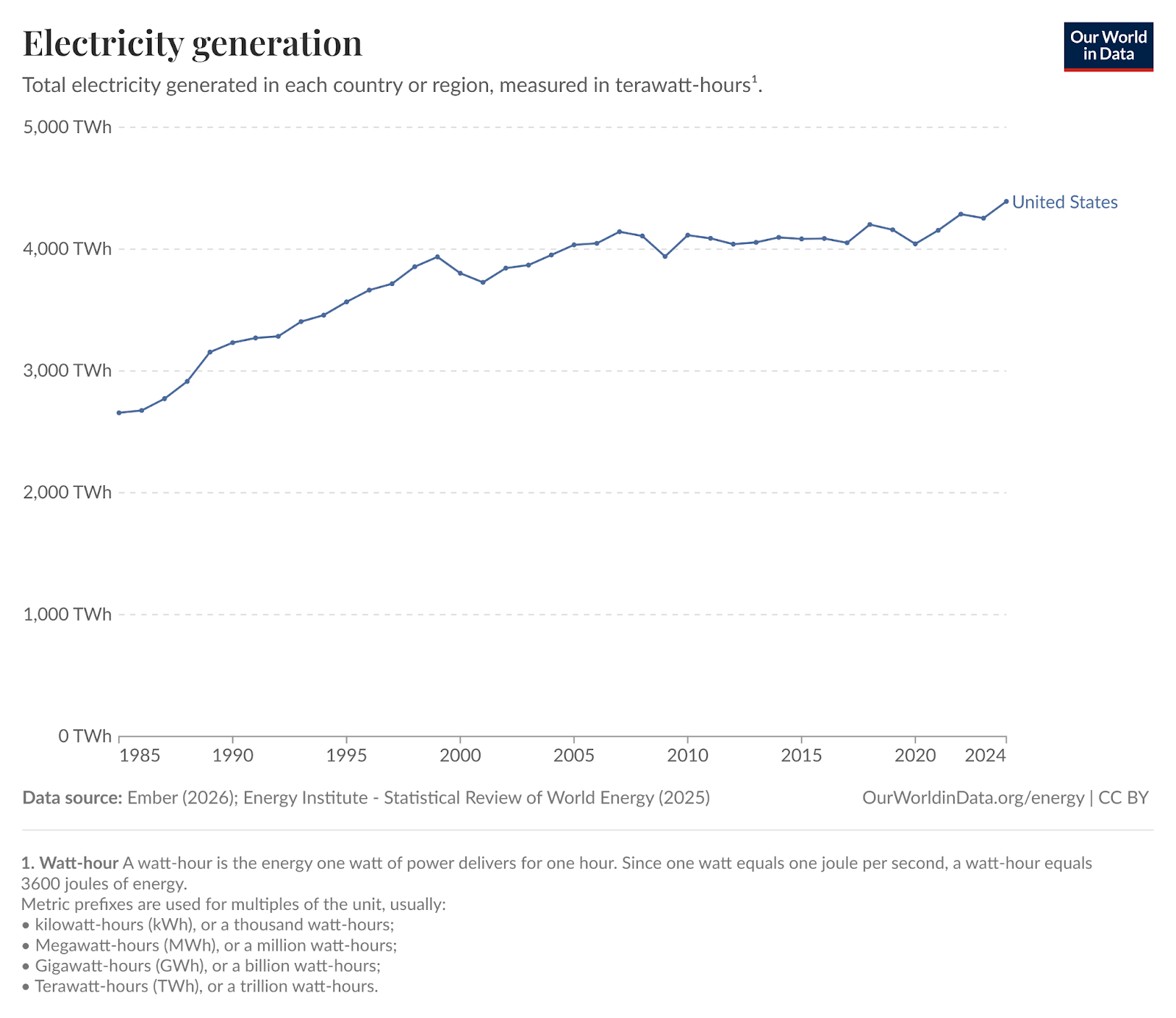

But demand for electricity specifically has started creeping upwards (note the difference in scale of the Y-axis and X-axis). Electricity represented about 16% of primary energy consumption in 2024.

In 2026, this growth is in the news because AI data centers are accelerating demand even more, but demand has been growing since 2018. Starting around 2012, EVs shifted demand from fossil fuels to grid-distributed electricity

The result is intense demand for all components of the grid, including the basic components needed to connect parts of the grid together. The biggest bottleneck for the last few years has been transformers.

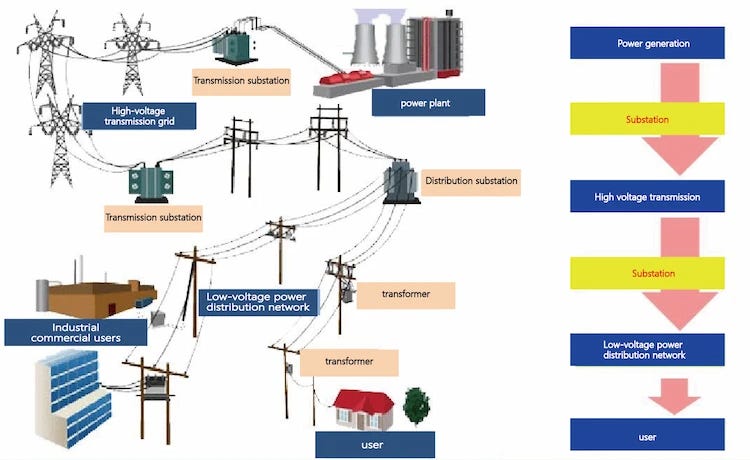

As their name suggests, transformers transform voltage, which is at one level in a given circuit, to a different voltage in another. Transformers connect different parts of the grid where different voltages are needed. Each connection requires a specific kind of transformer, so essentially every power cable is connected to either a generator and a transformer, a load and a transformer, or between two transformers. This means that there are a lot of transformers on the grid and there are extreme design limits to what can be done without them.

There are two common kinds of transformers: high-voltage transformers and distribution transformers. Power plants generate immense amounts of power. But to get to the devices that use electricity (known as the load), engineers have to pick the best way to get it there, balancing the cost of the equipment with the efficiency of transmitting and safety of the relevant system. By far, the most efficient way to send energy is via high-voltage transmission lines, operating from 69 kV up to 765 kV in the US. Transmitting power at high-voltage is efficient but super dangerous. The higher the voltage, the more likely electricity will arc to the nearest ground. It would also fry all your electronics, which in the US operate at usually 120 V and some power-intense appliances at 240 V. So high-voltage lines are treated like freeways to move huge amounts of power around. Like a freeway, there must be offramps and smaller streets to get to the destination (in this case, the load). Power leaving the transmission line is like getting off the highway onto a quiet street. Distribution lines attach to the transmission line and run to homes and buildings, operating at medium voltages (2.4 kV to 34.5 kV). The lower voltages are safer around more people and closer to the voltage residential and commercial appliances use, even if more power is lost at lower voltages. Getting it from the distribution network to a home or office requires another step down, from 2.4-34.5 kV to 120 V.

At each connection between different voltages, a transformer is required. Getting the power from the generator to the high-voltage transmission line usually requires a kind of high-voltage transformer called a generator step-up (GSU). Step-down high-voltage transformers are the offramps where power leaves the transmission lines for the distribution lines. Distribution transformers are what hangs on the lines outside your homes, converting the power to the 240V or 120V that home appliances use. Distribution transformers are by far the most common kind of transformer. The quantity of each kind of transformer in the US reflects a similar ratio of freeways to neighborhood streets. In 2024, NREL estimated there are about 10,000 times as many distribution transformers as large power transformers (60-80 million compared to 4,900 to 6,799).

Unfortunately, we do not have enough of any of these. This shortage poses unique risks to maintaining the grid, let alone expanding it to meet new economic demands. Each transformer represents an essential node in the network. If a node is lost and it takes years to replace, that part of the network goes dark. Transformers are lost all the time, from cars crashing into electricity poles to wildfires to intentional sabotage. In a future conflict, they are prime targets for drone attacks, with most networks completely immobile, exposed, mapped, and easily identifiable.

Thankfully, the feds have at least oriented themselves to the problem, even if investing in the grid is mostly a state and municipal issue. National Renewable Energy Lab estimates “distribution transformer capacity may need to increase 160%–260% by 2050 compared to 2021 levels to meet residential, commercial, industrial, and transportation energy demands.”

In 2023, Harris Williams, an investment bank, highlighted six drivers of transformer spending:

Aging infrastructure (as noted above by NREL)

Grid resiliency (i.e. having multiple connections between generation and load and being able to quickly replenish downed lines due to wildfire, sabotage, etc.)

Legislation driving more demand via subsidization

Renewable energy generation driving new kinds of supply

High-growth end markets (like AI data centers and electric vehicles)

Reshoring initiatives to do more domestic manufacturing

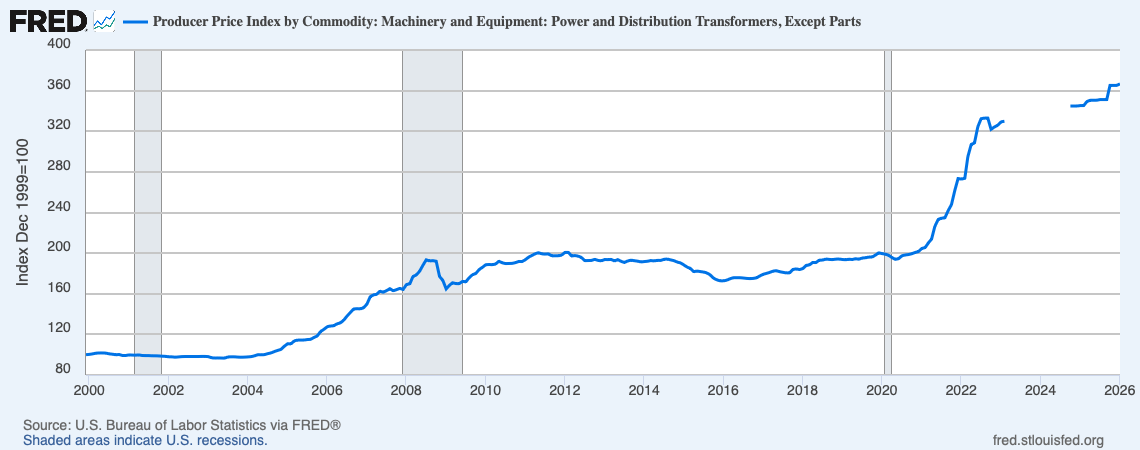

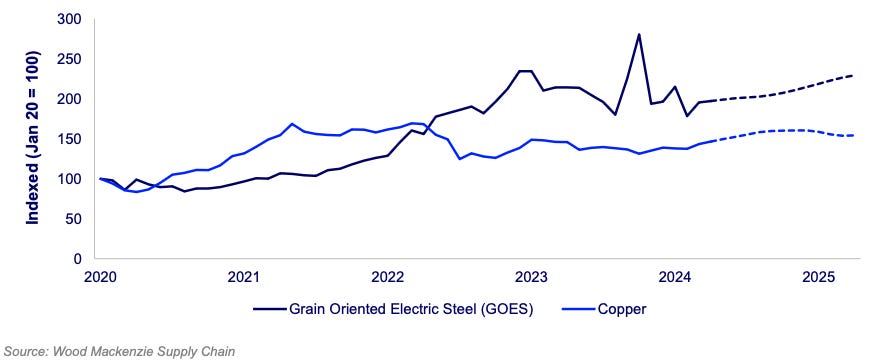

More demand without more supply had its textbook effect: the remaining transformers are even more expensive. Prices are up ~4x since the 2000s…

…though utilities should be willing to pay even more, given the deadweight loss to the economy. To recap, there are secular trends driving an increasing need for transformers. The demand is structural and sustained. Yet, six years on, prices and lead times stay high. Classically, price is the best signal to entrepreneurs to invest in more capacity here. Yet as of 2026, no new supply has come online in the US.

So why hasn’t supply responded? The answer is locked inside the transformer itself.

An Unfortunate Series of Moggings

Mechanical engineers such as myself love mechanisms, spinning gears, levers, and moment arms that put people directly in control of the machines. Yet, deep in our heart, we know that moving parts are the source of most trouble. A device that can do its job without moving parts is a universally superior design. No gears, no problems. In the vernacular, solid state devices mog devices with moving parts.

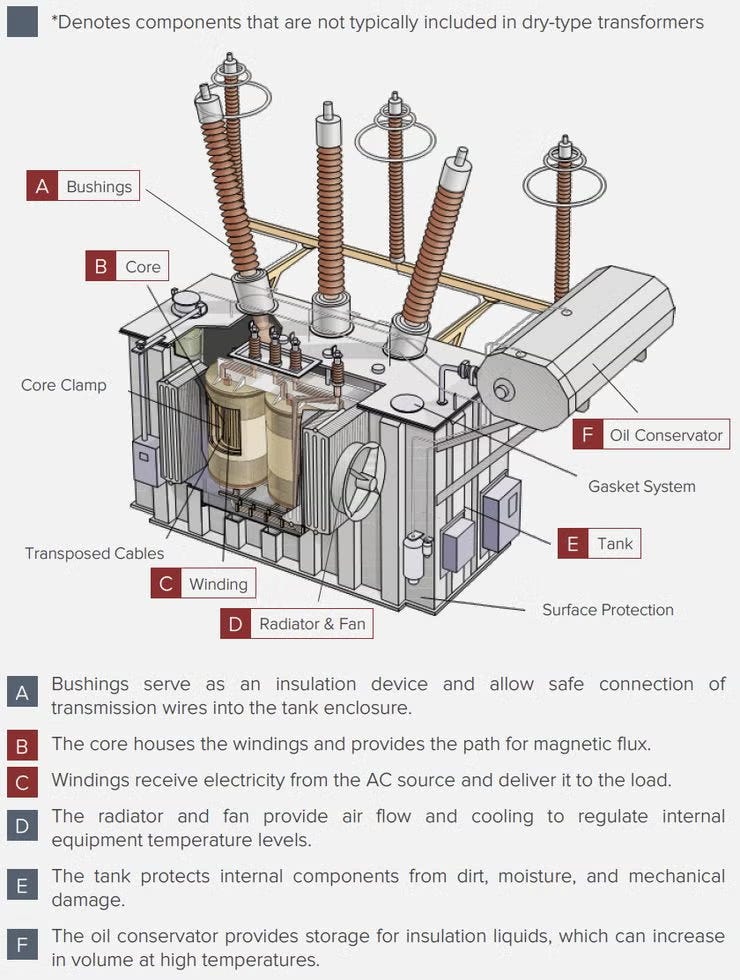

Transformers are fairly simple devices with few moving parts. The actual act of transforming voltage takes advantage of electromagnetic induction between two coils (usually copper or aluminum) attached to a core, a big slab of electrical steel. In operation, no parts move. The only moving part on most transformers is a switch that can be thrown manually or in some cases automatically to disable the transformer. These devices have been perfected with all extraneous parts ablated over decades of iteration.

Yet, transformers have a dirty secret.

Most of the components are pretty common: copper or aluminum, oil if used, and switchgear are all commodity devices. Electrical steel is what is causing the problems. Electrical steel has been produced for over 100 years. Sir Robert Hadfield of England created silicon steel in 1900. In 1934, Norman P. Goss patented a method for producing electrical steel with a grain that strengthened its effect. Today, we call these flavors of electrical steel grain-oriented (GOES) and non-grain-oriented (NOES). GOES is the most common in transformers because of its efficiency, while NOES is more common in motors due to the uniformity of its magnetic field. What makes GOES efficient is its purity, which requires fresh steel.

The fate of fresh steel in the US is best encapsulated in the name “Rust Belt”. What killed fresh steel in the US was economics. In the 1960s, Nucor introduced the electric arc furnace (EAF) mini-mill, which used plentiful recycled scrap steel to outcompete most of the aging, unionized steel producers using blast furnaces to make fresh steel. Yes, Nucor mogged Bethlehem Steel. While economics killed fresh steel, environmentalism ensured it would not come back. Blast furnaces require huge amounts of energy and release about 2.33 tonnes of CO2 for every 1 tonne of steel. Fresh steel would have to come from developing countries with low overhead, cheap energy, and either indifference towards climate change or accepting carbon release to preserve critical industries. You-know-who was front and center: as of 2023, China had 56% of global production. But making GOES is well understood and many other countries preserved their production, including Japan, Russia, Germany, and South Korea. In the US, there is only one producer of GOES: Cleveland-Cliffs in the Butler Works facility in Butler, PA. Butler Works produces about 250,000 tons per year across two facilities. North American consumption is approximately 539,000 tons as of 2022. The US is once again mogged by deindustrialization. But this was just the first of several own goals.

Forcing the Future

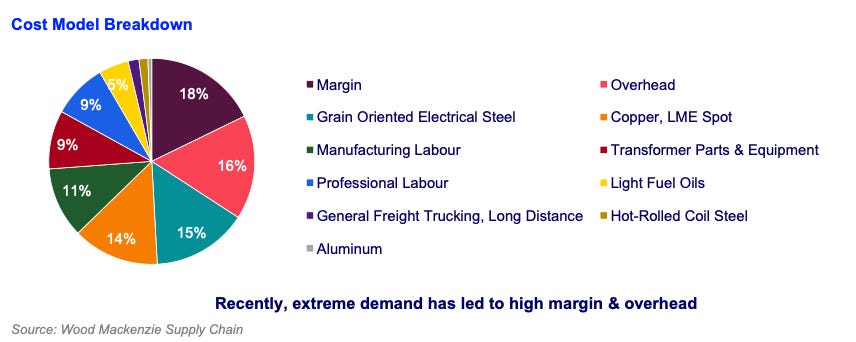

Six years of high prices should have drawn new investment. It hasn’t. International players should be filling the void, yet they are also delaying expansion. GOES requires precise metallurgy which is a significant barrier for commodity steel vendors to match their quality or the cost structure. A GOES factory can run into the billions and take over 5 years to build and commission. The customer base is relatively small and highly concentrated among transformer manufacturers, creating significant go-to-market risk. The market is small and the bet is enormous. The payback period for a GOES facility can take 10-20 years to recoup the investment, requiring high confidence demand will remain high and no one will create a substitute during that time. This fear is borne out by other bottlenecks in transformers, where even producers that can get enough GOES cannot find enough skilled labor to wind copper. A transformer is physically mostly GOES and copper plus a decent amount of labor.

Those copper wires are almost entirely wound by hand, resisting automation because customers refuse to standardize their designs. Finally, steel is always subject to trade policy risk, which makes it difficult for non-US manufacturers to be sure they will have continued market access and also makes US producers unsure if they will face cheaper imports over the next two decades. Of course, China wants to own their future and continues investing in their own GOES supply. In the US, every entrepreneur that has looked at this has run away screaming, even more than they usually do when trying to build a steel mill in the US.

In fact, GOES isn’t the only option. In the 1970s, Metglas created an amorphous alloy that is even more efficient. Metglas’ brochure claims that, “Compared to silicon steel core transformers, amorphous core transformers will have 50% lower losses at 20% load and 32% lower losses at 30% load“.

The rest of their brochure highlights the total cost of ownership of such a system, which is a business’ way of telling customers not to overreact to the sticker price. Amorphous metal itself is more expensive and the manufacturing process is subscale. In 2021, Metglas estimated they had sold 4,000,000 transformer cores (estimating the total number of distribution cores in the world is tough, but Gemini puts the US alone at 80,000,000). In 50 years of operation, it had achieved 5% market share.

To recap the situation in 2020, power demand from the grid was going up in the US from about 0% to 2% annually. The pandemic hit, causing the usual supply chain disruptions but the real impact would come in 2021: inflation. Inflation ripped through steel, copper, and specialized labor, sending prices up. The backlog grew. But the world needed more transformers, so prices and lead times grew. Without more GOES and more specialized labor, the supply chain would just have to grind through its backlog.

In February 2023, the Biden Department of Energy saw this supply crunch as an opportunity—to ban GOES. Hanlon’s razor applies here: the DOE didn’t attempt to ban the main BOM component for 95% of transformers on the market out of malice. It ran the only playbook it had: raise efficiency standards. For generations, DOE bureaucrats have only been asked to reduce consumption, not manage a growing power load. The DOE still had to show their latest mandatory efficiency increase had a business case. This exercise is functionally a political tool to see how much cost can be borne by the electorate, determining exactly where the regulatory ratchet of efficiency standards comes to rest. Amorphous metal represented a way to support grid growth due to electrification of the economy with EVs and heat pumps with a domestically produced, more efficient, less CO2-intensive metal. The Biden Administration saw this as a win-win.

That helps to explain why, even though the DOE had many policy tools available, including subsidization, they actually chose new efficiency rules that de facto banned GOES and would only allow amorphous metal cores in distribution transformers. DOE 10 CFR Parts 431 is 448 pages long. Mercifully, it puts its proposed efficiency table at the beginning. That table reads as “no more GOES” with another 400+ pages of why that supply shock impacting 95% of the transformer market won’t be a catastrophe.

One year later, the plan was dead. Remember Cleveland-Cliffs, the only US producer of steel? Their plant is unionized. Foreshadowing the growing rift between union workers and the Biden admin, they went to war with the DOE to protect their plant. By April 2024, the DOE had relented and Secretary of Energy Granholm had to do an apology tour, mogged by the union.

Yet the damage was done. No one has built additional amorphous facilities, and no additional GOES suppliers have come online in the US. It’s easy to see why there has been no investment in either commodity: plants often count on 15 year lifespans to generate any significant return. Even with increased demand over time, you have to compete with a globalized product in a market where one political party just tried to ban one of the two options. Will they try again soon? Will the other party try to ban the other option? In that environment, there is no safe investment, so no one makes any. Somewhere in its 448 page tome, DOE bureaucrats insist a GOES factory has options to pivot into other markets; the market’s silence says otherwise.

Bad Energy

The cumulative damage shows up in lead times.

Every month on that table is a month where a hospital can’t add backup power, a school district can’t connect rooftop solar, and a new housing development sits dark. The shortage isn’t an abstraction — it’s a tax on every project that would make daily life better.

By 2024, the market was starting to work through its backlog. Prices were high, but lead times started to return to normal. In principle, all the government had to do was nothing and the market might have corrected.

Reader, the government chose against doing nothing.

To incentivize domestic production, the government did tariffs. Steel, especially foreign steel, especially Chinese steel, was the first to get hit. GOES is subject to a 25% tariff when imported in raw roll form. Copper itself has a 50% tariff thanks to Section 232. But in global whack-a-mole supply chains, most suppliers dodged the tariff because laminations and cores are not tariffed, creating a perverse incentive to move more processing offshore.The tariff punished the raw material and rewarded the runaround. (More recent tariffs have threatened to patch this, and match the 50% tariff on copper.) Meanwhile, Cleveland-Cliffs celebrated the tariffs and promptly charged more for the same mid-grade GOES.

In 2025, the energy research organization Wood Mackenzie estimated the US distribution transformer still had a 10% supply deficit of distribution transformers and a 30% supply deficit for large power transformers. US power prices continue to climb.

Free Electrons

The Kardashev scale models civilizations based on their energy consumption because it is literally a measure of how much can physically be done. In the age of AI, it has become a measure of how much mentally can be accomplished too. The stakes are high, and the pressure reveals what you really believe. (Why else would someone ban supply in a crisis?) It compels institutions to be the most extreme versions of themselves, endorsing galaxy-brain attempts to spur domestic production that stops it dead in its tracks. Worse, no one seems to have acted like it was a crisis. Even worse than that, there is no feedback mechanism besides general discontent with affordability. Today, headlines blame datacenters for high energy prices. Yet there are decades of hairbrained schemes that haunt the supply chain with the realized costs and opportunity costs of their mistakes. In his book Breakneck, author Dan Wang labels the US a society of lawyers and China a society of engineers. Situations like transformers are a case in point.

Increasing use of energy per capita is the best way to improve and enrich humanity, and increasing electrification is the best way to do it efficiently and taking advantage of renewable energy sources. These demands will continue to grow, even though they radically outstrip current supply. Fortunately, innovation and policy options are both available.

There will be progress in the form of innovation. First, Hertha Metals is attempting to make fresh steel here in the US with an innovative new process that is cheaper, less energy intensive, and less carbon intensive. I wish them all the success in the world. Second, solid state transformers (SSTs) are poised to revolutionize distribution transformers. Considering transformers already have essentially no moving parts, solid state transformers have a rather silly name, but the benefits are real (see Drew Baglino’s writing on SSTs). They are more efficient, smaller, and give greater control. The control piece makes for better overall power quality and enables bi-directional power transfer. Traditional distribution transformers are optimized for sending power from transmission to load, but with bi-directional power transfer, homes, vehicles, and batteries on the distribution network can pump power back into the grid when needed (see Justin Lopas’ exciting new startup, Base Power, built around this idea). These innovations will help expand the solutions, but the US is wasting the solutions it has.

Policy problems require policy solutions. Standardizing distribution transformer designs on principles allowing for easy automated manufacturing would instantly unlock more supply. Asking DOE bureaucrats not to commit industrial suicide is trickier. Reforming the Department of Energy would probably require fewer mandates instead of more: maintaining efficiency standards is tacked on to their core responsibility of maintaining the nuclear weapons arsenal. Give somebody else a mandate to grow the grid, hold high efficiency standards, and keep prices low. We expect the Federal Reserve to use monetary policy to achieve maximum employment and stable prices, surely we can do this for the grid. Moreso it is a chance to reset the culture and build a culture of progress. And of course, tariffs haven’t changed anyone’s calculus on domestic production of GOES or transformer assembly. It is too simple to make elsewhere and too complicated to make in the US. Stories like this are endemic to the US industrial base.

I wish it was not so familiar: the professional building class waits for things to get bad enough before some sicko runs towards the problem instead of easier money. Trust in the institutions that manage the infrastructure powering daily life erodes. The steel mills that produce GOES do enough to survive, afraid they will lose their home market let alone attempt to compete globally. The regulators make the perfect the enemy of the good, freezing investment when we need it most. Trade policy manages to push prices up and encourage foreign sourcing but not domestic investment. Together, it represents a long slouch towards cyberpunk, a future state defined as high-tech, low-life. It starts with mismanagement of state resources only addressed through private innovation. Private innovation is the only escape from a web of incompetence and perverse incentives, slowly becoming necessary to sustain civilization as trust in institutions erodes. While I celebrate innovators and am grateful the situation can improve, this scenario is not a triumph of the private sector over the public. The trouble with transformers is a story of wasted time, energy, and treasure to serve select interests at the public’s expense.

Thanks to Sam Enright, Elizabeth Van Nostrand, Andrew Miller, and my wife, whose beauty and intelligence is unmatched, for reviewing drafts of this post. Any mistakes are my own.

Id never read about what transformers are - I know there is one in downtown toronto that every so often is knocked out of commission by a squirrel, leading to a power blackout, and Ive wondered how the system can be so fragile

I had to put some things behind the paywall and unfortunately the mechanics of a dramatically improved piston engine was one of them.