The CHIPs Act Rents the Future

Silicon Statesmanship #4

Previously: Facing Reality, Technoeconomic Pillars of Foundry, How to Grade the CHIPs Act

As laid out in the last post, the problems facing US semiconductors are:

Leading Edge Problems

Will the application of funds create the most advanced fab in the world?

Will the application of funds make the United States the most desirable place in the world to build future leading-edge fabs?

Given the goal of building more capacity at a level beyond what China is believed to be capable of, how much capacity will be generated with the application of funds?

How will inducing supply affect its relationship with demand? How much risk is there of underutilization, accounting for the subsidy reducing costs?

Lagging Edge Problems

How much will the application of funds encourage domestic semiconductor production of mature nodes?

Will American semiconductor manufacturers be able to compete effectively in the global market for relatively commoditized silicon?

Will the application of funds fix the structural issues with lagging edge supply in a sustainable way?

The table is set. The terms and problems are defined. These tools offer everything we need to examine the implementation of the CHIPs Act and the kinds of results possible.

Problem #1: The Leading Edge

The CHIPs Act has always been primarily about maintaining access to leading-edge silicon. It is where Congress allocated most of the dollars ($33B of $50B total), and it is the source of most of the fears of economic and defense dislocation, due to either disruption in Taiwan or China simply outcompeting the Western world. The success of America’s foray into semiconductor industrial policy will be measured on how it impacts the leading edge.

The CHIPs Act Program Office elected to spread the money around to each of the existing players. Their guideline was 5-15% of the capital cost. Per Ronnie Chatterji at Statecraft:

5-15% of the capital cost was the guideline in the report we released in February. For a $10 billion fab, 10% of that, $1 billion, is a huge grant to subsidize some of these projects. Remember that on top of that, there'll be state and local grants, tax abatements, and the investment tax credit that they can use in the federal tax code.

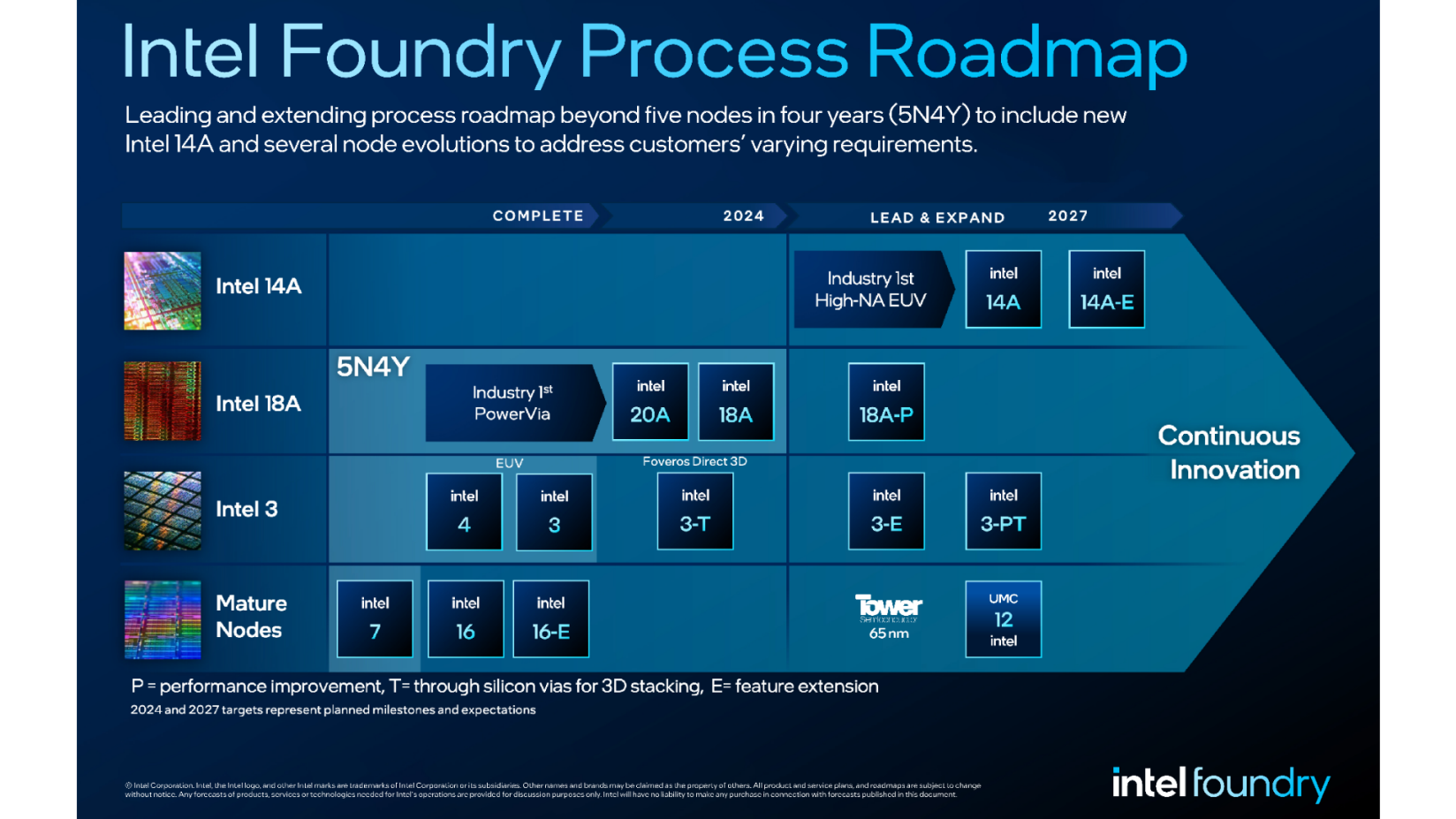

Intel has received the largest (non-binding, yet-to-be-finalized) grant of up to $8.5B from the CHIPs Act Program Office. Between 2024 and 2030, (1a) Intel could plausibly be building the most advanced foundry in the world. When it is scaling to production volumes, Intel 18A will at least compete to be the most advanced node in the industry. But money can’t fix their problems. In fact, Intel has had the resources to pursue leading edge processes for decades. In the last 10+ years, Intel has been limited by their own culture and poor execution. Recently, Intel made headlines for all the wrong reasons after posting a terrible quarter. While confirming hardware issues with some of their x86 products (i.e. the execution issue wasn’t on the manufacturing side that is relevant to the CHIPs Act), analysts speculated that there were also yield issues with the manufacturing tech. Intel was quick to add that their most recent node for Foundry customers, Intel 18A, powered on (August 2024) to give a semblance that the manufacturing side is in order. For this CHIPs Act funding to be considered a success, Intel must continue their transformation, executing on both the technical dimension of making leading edge processes and transforming their business to include a foundry trusted by US chip designers. Transforming their business would likely require opening their process to collaboration with key customers, increasing investment into their IP ecosystem, and adopting a more customer-centric technology development approach.

Meanwhile, (1a) the investments in TSMC and Samsung will not produce the most advanced fabs in the world at their time of construction. Rather, each company will be re-creating a node they have already successfully introduced in their home country 2-3 years before it comes to the US.

Most Advanced Process Node by Company by Country by Year

{kind=link}

(1b) Structurally, not much is different in building leading edge nodes in the US after the CHIPs Act. TSMC indicated their costs are 5X the cost to build in Taiwan, and it is unclear if this one-off investment will lead to any sort of experience curve improvements. Industry and government are already highlighting the need for continued investment.

(1c) If the goal is to build more capacity beyond the 5 nm node that China is expected to achieve, these new fabs will count towards that goal. While exact numbers are not provided, Secretary of Commerce Gina Raimondo expects that, by 2030, these investments could produce roughly 20% of the world’s leading-edge semiconductors. This is a huge improvement over the present 0%. Presumably, the vast majority of the remainder would be in Taiwan with other possible fabs in Japan and Europe. In my own estimation applying some industry math that $20B in Taiwan gets you roughly 100,000 wafer starts per month, the US fabs would have anywhere from 210-540,000 wafer starts per month with these fabs online. (1d) Given the scalable investments and milestone-based approach to rewarding grants, these targets indicate supply can be carefully managed. Meanwhile, the smaller scale of these fabs versus so-called GigaFabs in Taiwan guarantee their unit economics will be worse.

Problem #2: The Lagging Edge

(2a) Considering the entire CHIPs Act enables $50B of government spending, their grants here are limited to a $1.5B award supporting GlobalFoundries and a few hundred million dollar-range grants to key defense and automotive vendors. (2b) GlobalFoundries and possibly Texas Instruments, who indicates their application is still pending, compete in global markets. However, outside those two, it seems unlikely any other US-based lagging edge manufacturer will be competing aggressively outside US markets. Again, it seems this funding is not intended to enable domestic manufacturers to compete more effectively globally; rather, it is to ensure domestic supply is available for national security purposes. (2c) Ultimately, there is no easy answer for the broken business model in the lagging edge besides subsidization, and Congress clearly prioritized investment in the leading edge with 2/3 of CHIPs funding. Now, legislators, regulators, and the lagging edge vendors await a flood of lagging-edge chips from China’s $45B investment in Chinese domestic competitors.

Grade: C

The CHIPs Act Program Office took essentially 18 months to decide to subsidize the status quo. This strategy gives them some key wins. With some luck and Intel’s execution, the US may be home to the most advanced fab in the world once again—though it remains to be seen if they will become a foundry the industry uses. CHIPs Act investments ensured there are advanced fabs built in the US again (for now). CHIPs’ policies do not address the structural issues with locating fabs in the US; they are simply subsidizing the alleged 5x higher cost of construction than Taiwan. The CHIPs Act had relatively little capital to deploy towards the lagging edge, and it was deployed conservatively with an eye on key suppliers.

Isn’t the point of industrial policy to do something that would not happen otherwise?

The CHIPs Act bets are understandable and defensible to the American public, but I am left with the feeling that the US has rented the future. Yes, the fabs built here will stay here. But it does not feel that gravity of the industry has shifted. Without CHIPs Act 2, it seems just as likely the next leading-edge fabs will go back to Taiwan. When asked about the long-term implications of government and industry planning fabs, during an interview with Fabricated Knowledge Hassan Khan of the Department of Commerce stated that the intent of each award was to be the “marginal dollar for the majority of these projects.” He continued, “we’re not trying to create something that would not happen otherwise, and like an unnatural way.”

There is a critical difference between “should we build a fab” and “should we put the fab we want to build in the US or in Taiwan,” but isn’t the point of industrial policy to do something that would not happen otherwise? Interestingly, the US is one of the few countries pursuing an industrial policy of subsidizing multiple vendors. In contrast, both Taiwan and now Japan have centered their industrial policy on an alternate approach: putting all their subsidy behind a national champion, giving them the best possible resources to compete globally and own their future. More on that next time.

Hi Rob, Great summary. Just one nuance: I think the challenge for Intel goes a bit beyond having a foundry that is trusted by US customers - it's about having a foundry that is competitive with TSMC which will require getting leading edge nodes working , cost and yield competitive and having processes that work as well for customers. And all this needs to be so good as to overcome a track record that is not as good as TSMC's. Of course this assumes that there is no political intervention to push customers away from TSMC and to Intel.